Overview

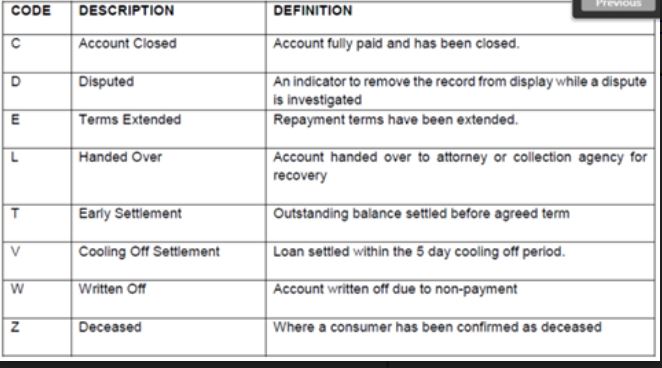

Code C: Account Closed and we also use this code for accounts marked written off.

Code D: when the credit provider suspects fraud and wants the account to be removed from display, while he investigates. If the account is found to be correct, he would then need to submit a manual amendment directly to all bureaus to bring the account back into display.

Code E: Dee: All status codes I listed is applicable to account types M and P, including E. This is applicable when the credit provider grants the consumer extended terms and/ or restructures his debt. When submitting status code E, payment type 06 becomes mandatory.

Code L: Clients needs to be explained the importance of correctly using status codes as this is part of the data specification and thus part of compliance for them. Incorrect use of status codes means inaccurate data submissions and this can be reported to the regulator.

Code T: is left for interpretation as to how many

days prior to the term being reached is considered early settlement.

Personally, when asked this question,

I say if the account has been settled 30 days or more before the term reaches an

end. But it is up to each credit provider to decide the use.

Code V: Not currently submitting. We are adding this for the next update. Dee: When is the next update due.

Code W: should be used when credit writes off an

account and once the Code W is submitted there account must no longer be

submitted to the bureaus.

If a Code W was submitted and the consumer

pays the full outstanding amount then only Code C can be submitted provided it

is still within 36 months of the last submissions.

Code U is used to remove

the Code L status code when there is a partial hand over, so the credit provider

only hands over only the amount that is in arrears and once the arrears

is paid

then the account is back in good standing and the consumer continues to pay on

the account until the end of the term is reached.