Overview

Regulation 19(13) in the National Credit Act 34 of 2005, stated:

“A credit provider must submit credit information to the credit bureaus in the

manner and form prescribed by the National Credit Regulator”.

Layout

700v2 Specification And Process Rule Document

Version 2.8

Publication

Date: June 2015

Page 40:

Current Balance:

The balance of

the account as at month end.

No future costs fees or interest is to be

reported.

Instalment:

The amount which is expected

from the consumer in order to ensure the account will remain current.

All

values reported must be as at the reporting month and not include any future

billing which are not being sought from the consumer in the month of

reporting.

Exception: If a deferred payment type and date are populated then the instalment should reflect the expected instalment at the deferred date (thus may include future insurance, costs and interest to the point of the expected payment).

Overdue:

Total value which has not been

received within the agreed repayment period (monthly, weekly, annually)

etc.

This value should include overdue costs, overdue insurance and overdue

Interest.

Where there is an agreed Contractual instalment for the accounts

type the overdue contractual instalments or portions thereof should be reported

as overdue

Months in arrears (Field 37) must be supplied as actual months

past due

If months in arrears is populated an overdue balance should be

expected

DATA FORMAT PRESCRIBED BY THE NATIONAL CREDIT

REGULATOR

Category 3: Product Descriptors

Personal Loan: Loan

granted to consumer for use in his personal capacity where the loan is to be

repaid over a term greater than 1 month.

Category 5: Current Account Status Codes and Status

Date

Account Closed: Account fully paid and has

been closed.

Disputed: An indicator to remove the record

from display while a dispute is investigated. CURRENTLY a MANUAL

process.

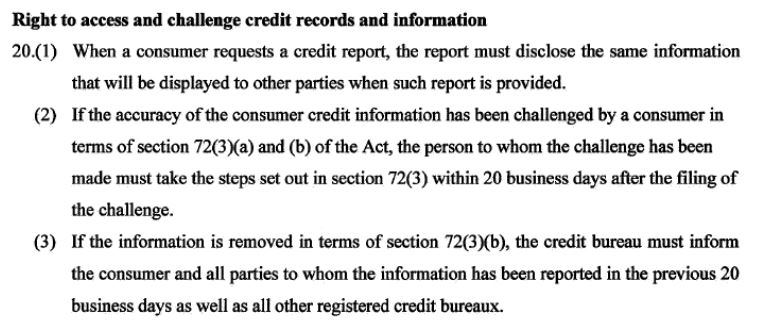

NCA Regulations 20.

Handed

Over: Account handed over to attorney or collection agency for recovery

but still owned by the Member. May only be used in Monthly files. Send when loan

status on LMS is Non Performing.

Early Settlement:

Outstanding balance settled before agreed term. This will be sent as a CLOSED

Status.

Settlement of Adverse Arrears: Where the obligation

under the agreement relating to the adverse has been settled, but the account is

still active. This will be sent as a CLOSED Status.

Cooling-Off

Settlement: Loan settled within the 5-day cooling off period. Sent when

loan status in LMS is cancelled. This will be sent as a CANCELLED

status.

Written Off (Adverse Code): Account written off due

to non-payment. May only be used in Monthly files. This will be sent as a CLOSED

status.

Deceased: Where a consumer has been confirmed as

deceased. MAXMONEY does not sent this information. The bureaus obtain the

information.

NLR Decommissioning

Dormant Micro

Loan Accounts

It was resolved by the members of the CBA that dormant

micro loan accounts, which meet the following criteria, must be updated by

members of the CBA to reflect as a closed account – i.e. status code “C” on the

date the action took place (status date):

• All dormant micro loan accounts

that reflect an open date of older than 6 months; and

• no update has been

received from the data supplier in the last 6 months; and

• the data

submission is up to date; and

• the account is reflected as being either

current or 1 months in arrears; or

• the account is reflected as being more

than 1 month in arrears, but the term of the credit agreement has expired.

•

Dormant micro loan accounts may not be amended where the account status is

reflected as either a W, I, J or L.

For purposes of this policy directive the

following phrases bear the following meanings:

• A micro loan account is

defined as an unsecured loan account hosted by the credit bureaus where the

account type is one of the following: 1, 2, 3, 4, J, K & M.

• A dormant

micro loan is an open/active unsecured loan (account types 1, 2, 3, 4, J, K

& M) where no payment performance information has been received from the

credit provider for more than six months.